Global 3D printing hardware revenues saw 'robust growth' in the first quarter of 2026, according to the latest figures published by CONTEXT.

A +32% year-on-year (YoY) gain in total 3D printer revenues was fueled by success from entry-level (printers priced below $2,500) and industrial (priced above $100,000) segments, which saw +39% and +18% increases in printer unit shipments respectively, resulting in +54% and +23% surges in revenue.

Challenges, however, persisted for midrange ($20,000–$100,ooo) and professional systems ($2,500–$20,000) which saw shipments drop by -6% and -22% YoY due to competition from lower cost material extrusion-based printers including Bambu Lab, Creality, Elegoo, and Anycubic. These four vendors made up 88% of all printers shipped globally during the period.

It's not all bad news, though, as polymer powder bed fusion (PBF) systems in the midrange category saw shipments up +48% YoY with new technology offerings such as Formlabs's Fuse X1 and HP's sub-$60K Jet Fusion 1200 building out this subcategory. CONTEXT also says that the professional class should expect a boost in coming quarters from new technologies including full-colour material jetting an composites, the latter due to Stratasys' planned acquisition of Markforged.

"The current market presents a disparate demand outlook," said Chris Connery, VP of Global Analysis at CONTEXT. "While some vendors report exceptionally strong demand, especially related to global conflicts and defence initiatives, others report challenges associated with the many unknowns including ongoing global conflicts, fears of rising inflation, higher interest rates impacting capital investments, and a sluggish European economic environment. However, the strong performance of the Industrial sector, marking its third consecutive quarter of growth after two years of declines, is a clear indicator of the technology's continued integration into volume production.”

Other key takeaways from the latest report include:

- Nine out of the top ten global vendors of industrial systems shipped more units in Q1-26 than a year ago.

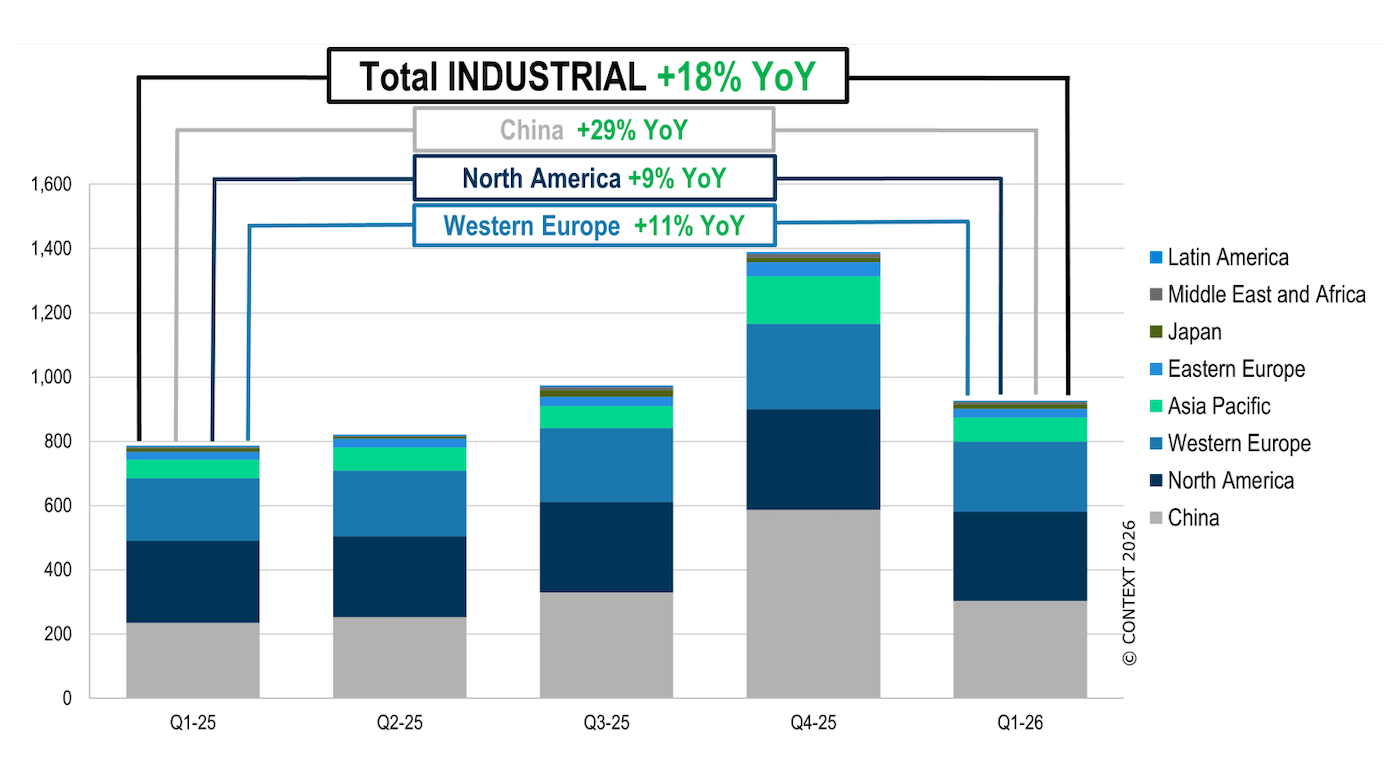

- While China remains the largest market - mainly due to domestic sales - industrial shipments were up across all major regions: China +29%, North America +9% and Western Europe +11%.

- 81% of industrial metal shipments were PBF systems, with shipments up +24% YoY. Just look at EOS's recent sale of 30 systems to Beehive Industries - the company more than doubled its sale of metals systems compared to a year ago.

- Nikon SLM Solutions also shipped more of its large-format multi-laser NXG systems than ever before, a +42% YoY increase in unit shipments.

- We could, however, see a limited supply of industrial metal systems in the West due to high demand outstripping supply.

- Farsoon and BLT cited strong demand from the 3C sector, mostly for the production of titanium mobile phone components.

- Industrial polymer system shipments surged +31% YoY, heavily skewed by a huge acceleration of shipments from Carbon.

- Polymer PBF shipments were up +30% from a year ago, largely due to HP and EOS, which saw shipments rise +100% from a year ago.

- Drone production is driving much of the growth for industrial material extrusion and PBF systems.

- Entry-level systems alone accounted for +54% of all 3D printing system revenues in the period.

- The strongest entry-level YoY shipment growth came from Flashforge, which saw printer shipments jump over 120%.